I mean, just look at these stories. It’s a downpour. In India, Australia, the United States, no matter where you look, or which crop, the climate-change-is-killing-agriculture narrative is exactly the same. Only details differ.

Just last week, the UN Food & Agriculture Organization (FAO) released its long-awaited deep dive, reported here and here, into the connection between extreme weather and food production in every region of the world from 2005-2015, and the findings should be enough to make every city manager everywhere scramble for solutions.

Darn near $100 billion in crop and livestock was lost, half of that in Asia, home to half of the world’s population, but also home to the bulk of future population growth. The other big surge is expected in Africa, today home to most of the world’s nearly 1 billion hungry people, the most climate-vulnerable of all.

But wait, it gets nastier. Exhibit 1 is this recent study that points to a 50% or so (“only” 25%-70%, it says) growth in food demand by 2050, given rising population, lifespans and incomes. For Exhibit 2, scroll down to the End of Food section in this review of the latest climate science by New York magazine, or check out this HBR story, and you’ll find the makings of an epic crunch.

The exponentially faster wave of storms, droughts, heat, fires, sea levels, and plagues forecasted by every reliable source for the coming years and decades, will lead to a significant decline in arable land, water and therefore food production precisely at a time when population and demand will skyrocket.

Considering we might overshoot 1.5ºC as soon as next decade and 2ºC shortly after that, triggering the acceleration of those climate impacts — you know those solutions city managers should be tripping all over each other to implement? Well, we need them yesterday.

The slow pace to date is, to be fair, understandable. The official UN acknowledgement of the 1.5-2ºC time frame and urgency happened only last year. Prior to that, as enshrined in the December 2015 Paris Climate Agreement, leaders were pointing to century’s end. So we thought we had more time.

We don’t.

It’s the cement envelope, stupid

So what are those solutions? They run the gamut, and all are being implemented to varying degrees. More farming in urban lots and rooftops. Less in distant rural farms. Better use of smart tech. More water conservation. Enhanced irrigation. Modern soil treatment. Stronger pest control. Greater reliance on greenhouse-grown food. Etc.

The common denominator is higher yields per acre and more reliable, resilient ways to get food to those who need it, particularly during or following a natural disaster.

But there is one important caveat.

If the food is produced outdoor in an open space, whether land or roof, rural or urban, none of these enhancements will actually protect it from a severe weather hit. The only way to do that, the most resilient shield, is to grow indoors, inside concrete walls that can resist storms, floods, heat, pests, and all manner of climate risks, hopefully even wildfires!

Sure enough, indoor farming, or harvesting on floor-to-ceiling vertically stacked racks and towers, is growing fast, expected to reach $6.4 billion in the next five years with a healthy 24.2% compound annual growth rate.

That is, no doubt, impressive, but the raw urgency of the moment, the epic clash, should produce meteoric growth not unlike that seen in the Google-Facebook-Amazon digital world, as it dawns on farmers, funders and policymakers that herein lies the most resilient source of food for the highest number of people on the planet.

To be sure, with total food production today in the trillions of dollars, indoor vertical farming is not even scratching…well, let’s just say it has a ways to go before it supplies a large portion of what we eat. In the meantime, traditional farming must, indeed, proceed with its own aggressive resilience agenda, as indoor vertical farming runs the cycle and expands.

Luckily for the world, there is a path forward that features more exponential growth than even industry executives are envisioning today.

Spotlight: AeroFarms

To discuss the prospect and challenge of rapid scale for indoor vertical farming, The Resilience Journal caught up with David Rosenberg, co-founder and CEO of AeroFarms, one of the industry’s clear leaders, with nine farms in several countries, including its flagship 70,000 sq. ft. farm in Newark, New Jersey, where the company grows 2 million pounds of leafy greens per year. AeroFarms aims for 25 facilities in five years, all in large-population metro areas.

TRJ’s exclusive sit-down with Rosenberg in this video turned into quite the unusual journey, as he takes us into the dynamics of “this exciting industry” and why it is poised for take-off.

AeroFarms is far from the only player. Others include fast up-and-comer San Francisco-based Plenty, which is wrapping up construction on its second farm, a 100,000 sq. ft. facility in Seattle, and Tokyo’s Mirai, which has big plans for Asia.

The Netherlands, long a leader in large-scale greenhouse farming, is making a strong push indoors, while long-time vertical mushroom grower Pietro Industries produces upwards of 20 million pounds in three large properties in Chester County, Pennsylvania.

Do a Google, YouTube or hashtag search of #verticalfarming, and you’ll discover countless others, mostly small, local concerns.

Not only is an indoor farm protected by concrete walls, but even when hurt by a weather event, the interruption is minimal compared to traditional farming.

AeroFarms, for one, has a blazing fast 14-15 day seed-to-harvest cycle, which produces 23-24 crop turns or harvests per year, compared to the average of three in traditional field farming.

“If there is a storm that knocks out power,” Rosenberg said, “with 23 harvests a year, if we have to scrap a harvest, that’s easier to manage than if you’re in the field and have three harvests and lose one. That’s painful. In a business with very low margins, it can be catastrophic.”

The coming boom

It is an industry buzzing with activity. Last year, AeroFarms, a certified B-Corp social enterprise, became a private-sector partner of the Rockefeller Foundation’s 100 Resilient Cities initiative, where one hundred city teams receive support from some 80 corporate and NGO partners and compare notes on the latest resilience trends and case studies.

“What we do [in 100RCs] is educate cities on the considerations to see if this is meaningful for you, and here are the considerations on how to accelerate it,” Rosenberg explained.

“We have a business development team that focuses on where to build farms next. Probably biweekly we have a city come to us to build a farm,” a fantastic indicator that interest is spreading.

Most signs, though, point to how far vertical farming is from being considered a mainstream part of city development.

The we-thought-we-had-more-time mindset regarding 1.5-2ºC, along with the early stage of the industry, means city officials have not yet launched the kind of aggressive incentivizing and promotion commonly deployed when they appeal to manufacturing, tech companies, hotel chains, start-ups and other economic-development segments.

In this case, they’ll be attracting indoor vertical farms to their metro areas, or nurturing the growth of local ones, to address the chronic food shortages and supply interruptions sure to mark every economy in a 1.5-2ºC world.

Given these fundamentals, it is only a matter of time, and likely not much, before cities awaken to the urgency, become aggressive promoting and competing for vertical farms, and trigger precisely the massive scaling of the industry that is now a requisite to becoming truly food resilient.

“This is a great place for public-private partnerships. The public sector can put incentives in place to drive innovation and food security,” and there are federal incentives in place in the United States, but those predate massive urbanization and are instead designed for rural field farming, Rosenberg explained. “They weren’t written with the notion of vertical farming. So from a legislative perspective, there needs to be a change to enable vertical farming.”

That said, “cities can incentivize,” and the industry stands ready to collaborate and define the path forward, he assured.

The 100RC platform is already creating such connections. Another increasingly popular pathway is ARISE, the private-sector collaboration arm of the UN Office of Disaster Risk Reduction, the agency behind the 2015-2030 Sendai Framework for disaster response.

The industry’s growth isn’t just driven by resilience and the interest of cities to enhance food security. Vertical farms are also responding — indeed, in some cases more so than resilience at this early stage — to consumer trends favoring natural and organic food and trend lines showing dramatic growth in the years ahead.

Both drivers have oiled an underlying ecosystem and market infrastructure that includes funding, distribution, technology and talent, with more sure to come.

So the industry is mature. The partnership platforms are in place. All we’re waiting for, it seems, is vision.

Did somebody say technology?

Of all those underlying enablers, perhaps none explains the timing of this phenom as the availability of key innovations.

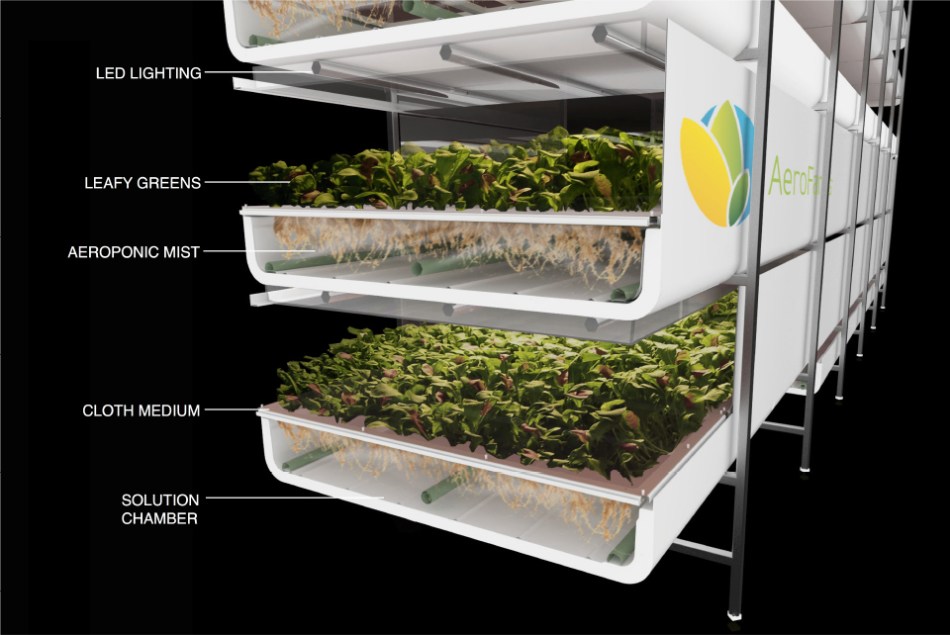

AeroFarms is called “aero”, for one, because of its unique aeroponic technology. Most vertical models feature aquaponic or hydroponic methods requiring vastly lower water usage than traditional farming, but where plants still sit on water-filled trays or otherwise receive nutrients from a water source.

With aeroponics, the plants are fed using an air mist that consumes even less water and provides the needed feeding and oxygenation.

Then there is the sustainability driver. Water is but one of the huge benefits on that front, the others being less use of land — anywhere from 350-400 times the yield from a given acre compared to traditional field farming — plus complete avoidance of pesticides, fungicides and herbicides, magnitudes lower food spoilage and waste, zero contamination of freshwater sources, no degradation of arable land, and the far lower need for carbon-emitting long-distance transport and industrial food production.

Along with the resilience, these sustainability gains weigh against the sole non-sustainable aspect of the industry: higher energy consumption than sun-and-rain-fed outdoor farming, though the energy consumption is at least partly offset by efficiency controls, LED lighting, and where feasible, solar and wind sources.

The LEDs are used, instead of the sun, for the light plants need to grow. The seeds are placed on a specially designed cloth instead of soil, yet another sustainable, resource-saving practice. Fine-tuned controls manage just the right combination of mist, light and other nutrients to deliver not just sustainability and savings, but also the taste and texture that has led to the company’s rapid consumer sales to date, under the brand Dream Greens.

To scale the company’s size and and with it its contribution to resilience, AeroFarms also plans to diversify beyond leafy greens.

“We have a whole team exploring other crops and figuring out when they can be commercialized. From a technology perspective, we can grow anything, but it has to make economic sense. By 2020 we should be launching our next very different category of food.”

In the end, this is an industry driven by the same no-choice paradigm behind all things resilience, because when it dawns on the cities of the world what little time they have before food security rules the headlines and renders other options at best unstable, at worst unavailable, it’ll be good to have the AeroFarms of the world, with proven models, high standards and management depth, right there in their neighborhoods, near their people, ready to scale.

Pingback: Finally! Mainstream consensus. Now, next-gen innovation…for 2050 adaptation – The Resilience Journal